The Dollar's Dilemma: America's Coming Policy Shift

Intro

Donald Trump's return to the presidency in 2025 will likely mark a decisive shift in US trade policy, but not in the way most analysts expect. While markets are focused on the prospect of higher tariffs and increased trade tensions, we believe the new administration's approach will be more sophisticated and potentially more effective than Trump's first-term policies.

The key personnel choices, particularly VP-elect JD Vance and Treasury Secretary nominee Scott Bessent, suggest an administration that understands the true mechanics of global trade imbalances. Unlike the previous focus on bilateral trade deficits and tariffs, there are indications that policy may target the root cause of persistent US trade deficits: excessive foreign capital inflows.

Both Vance and Bessent have demonstrated a nuanced understanding of global trade dynamics that goes beyond conventional wisdom. Vance has shown familiarity with modern trade theory that emphasizes the role of capital flows in driving trade imbalances. In a March 2023 exchange with Federal Reserve Chair Jay Powell, he questioned whether the dollar's reserve currency status acts as "a massive subsidy to American consumers but a massive tax on American producers."

Bessent, a veteran global macro investor, has explicitly argued for a different approach than Trump's first term. In Key Square's January 2024 Investor Letter, he wrote that Trump will likely pursue a weak dollar policy rather than implementing tariffs, noting that "Tariffs are inflationary and would strengthen the dollar--hardly a good starting point for a US industrial renaissance."

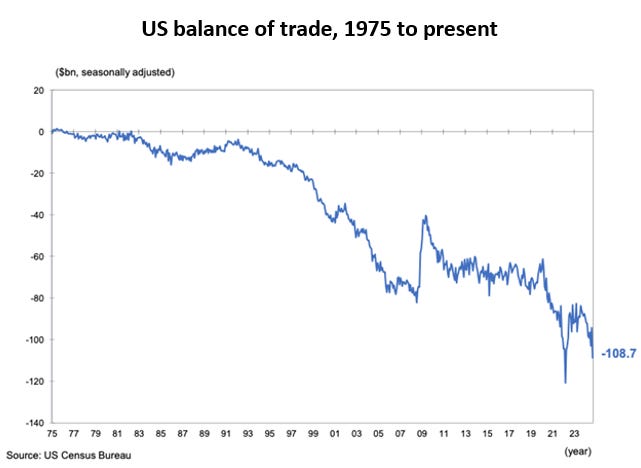

This shift in approach matters because previous attempts to address US trade imbalances have failed largely due to a fundamental misunderstanding of what drives them. The conventional view that US trade deficits reflect American overconsumption or lack of competitiveness misses a crucial point: in today's global financial system, capital flows drive trade flows, not vice versa. The persistent US trade deficit is primarily a symptom of excessive foreign demand for US financial assets, not American consumer behavior or trade policy.

In this report, we examine why targeting capital flows rather than trade flows could prove more effective at addressing global imbalances. We explain why attempts to reduce the trade deficit through tariffs alone are likely to backfire, and why a coordinated approach to managing capital flows might succeed where previous policies have failed. The implications for currency markets, asset prices, and global trade flows could be profound.

Understanding Global Trade Imbalances: The Balance of Payments Framework

To understand why the new administration's approach to trade policy might succeed where previous attempts have failed, we first need to examine how international trade and capital flows actually work. Most analysis focuses solely on the flow of goods and services between countries. However, this view captures only half the picture.

International transactions are part of a larger system that includes two types of flows: trade flows (the exchange of goods and services) and capital flows (the exchange of financial assets like stocks, bonds, and property). These two flows are inextricably linked through what economists call the balance of payments, which can be expressed in a simple but powerful equation:

Trade Account* = Capital Account

*The technical BoP identity is: current account = capital account, but we are using “trade account” in place of the “current account” for simplicity. It should be noted that the current account differs slightly from the trade account – a fact we can ignore for our discussion.

The balance of payments accounting identity tells us that any change in one side of the equation must be matched by an equal and opposite change in the other. For example, when Korean pension funds invest $1 billion in U.S. stocks, all else equal, U.S. net exports must decrease by $1 billion and Korean net exports must increase by $1 billion - despite this transaction having no direct connection to trade in goods and services.

Why does this relationship hold? The answer lies in the simple fact that when foreigners acquire U.S. dollars, they can only do two things with them:

1. Buy U.S. goods and services (affecting the trade account)

2. Buy U.S. financial assets like stocks, bonds, or real estate (affecting the capital account)

Therefore, when foreigners use their dollars to buy more US stocks or bonds, it automatically reduces US net exports of goods and services. Some might argue there's a third option - using dollars to buy commodities or assets from other countries. However, this merely transfers the dollars to new holders who face the same two choices. Eventually, all dollars must return to the U.S. to purchase either goods and services or financial assets.

This framework helps explain why many conventional approaches to reducing the U.S. trade deficit have failed. When we focus solely on trade flows - through measures like tariffs or export promotion - we ignore the powerful role that capital flows play in driving trade outcomes. In fact, in today's global financial system, it's often capital flows that determine trade flows, rather than the other way around.

One of the fundamental misunderstandings about trade imbalances—particularly why China runs a persistent trade surplus while the US runs a persistent trade deficit—is the assumption that these imbalances are driven by one country’s inherent production cost advantage over the other.

While production cost advantages do exist, they are not supposed to persist indefinitely in a properly functioning global trading system because trade imbalances should trigger self-correcting mechanisms that reverse relative production cost advantages.

In a properly functioning global trade and capital flow regime, persistent imbalances would self-correct. When a trade surplus country experiences excess demand for its goods and services, this should cause either its currency to appreciate or its relative inflation rate to rise (changes in relative productivity can also occur but this is slower and less directly determined by trade and capital flows). Both mechanisms increase the production costs of the surplus country relative to its trading partners, eventually reducing the surplus and rebalancing trade flows.

The critical question to ask is: Why haven’t currency values adjusted to rebalance the system? Why has the trade surplus currency (e.g., China’s renminbi) failed to appreciate relative to the trade deficit currency (e.g., the U.S. dollar)?

Once you understand that this lack of currency adjustment is a central feature of how the global trading system is supposed to work, you begin to see why the system is broken.

The reason the rebalancing mechanism has failed to operate effectively, and persistent trade imbalances have persisted for the past 40 years, is due to a fundamental distortion in the demand for currencies.

There are two distinct drivers of currency demand:

1) Demand for goods and services (trade flows).

2) Demand for financial assets (capital flows), which arises from the preference for holding or investing in a particular country’s financial instruments.

In today's financial system, it's this second source of demand - the desire for U.S. financial assets - that has effectively short-circuited the natural currency adjustment mechanism. Despite decades of large trade deficits, which should have led to dollar depreciation, the U.S. dollar has remained strong because of overwhelming foreign demand for U.S. financial assets.

The overwhelming demand for U.S. financial assets reflects structural features of the global economy, particularly policies in surplus countries that generate and export excess savings. These policies systematically suppress household income and consumption, forcing domestic savings rates far above what's needed for domestic investment.

Consider China, where households retain the lowest share of GDP ever recorded for a large economy. This isn't cultural thrift - it's the result of policies that transfer income from households to the corporate sector through currency undervaluation, financial repression, and weak social safety nets. The excess savings generated by these policies must be exported, primarily to the U.S. financial system.

This capital flow into U.S. markets comes through two channels:

First, public sector flows dominated in the 2000s and early 2010s as Asian central banks, led by China, accumulated massive dollar reserves. This policy-driven accumulation prevented natural currency appreciation that would have corrected trade imbalances.

More recently, private capital flows have taken center stage. As surplus countries generate savings far beyond domestic investment opportunities, private investors seek returns in U.S. markets. This shift from public to private flows hasn't changed the fundamental dynamic - surplus countries still export their excess savings, forcing the U.S. to run corresponding trade deficits.

These "beggar-thy-neighbor" policies effectively export unemployment and weak demand to deficit countries while preventing natural rebalancing through currency adjustment. The U.S., with its deep and open financial markets, has become the primary absorber of these excess savings, explaining the persistence of its trade deficits and decades of dollar overvaluation.

Capital Account Dominance: The Tail Wagging the Dog

Understanding why currency adjustment hasn't occurred requires examining how the nature of global financial flows has fundamentally changed over the past century. In the era when tariffs were the primary tool of trade policy - think of the infamous Smoot-Hawley tariffs of 1930 - trade flows dominated international transactions. The capital flows that did exist were primarily tied to trade financing, essentially facilitating the exchange of goods and services.

Today's world looks radically different. Starting in the 1980s, global capital flows exploded in volume and complexity, driven by financial deregulation, the elimination of capital controls, and innovations in financial markets. By the early 2000s, daily trading volume in global foreign exchange markets had grown to more than 100 times larger than daily international merchandise trade.

This transformation means that capital flows, not trade flows, now dominate in determining exchange rates and trade balances. While trade negotiators continue to focus on tariffs and market access, the real action is in the massive flows of capital seeking returns across global financial markets. These flows dwarf the impact of changes in trade policy, which helps explain why traditional trade tools like tariffs have become less effective at addressing trade imbalances.

This understanding of how capital flows dominate trade flows isn't merely theoretical - it explains why many trade policies fail to achieve their intended effects. During Trump's first term, we predicted that tariffs alone would fail to reduce the U.S. trade deficit. In fact, we argued they would likely increase it. This is exactly what happened.

Why? Because tariffs triggered two responses that increased demand for U.S. financial assets. First, heightened global economic uncertainty drove safe-haven flows into U.S. markets. Second, foreign central banks loosened monetary policy in response to tariffs, widening interest rate differentials and attracting yield-seeking capital into U.S. bonds. This surge in capital flows into the U.S. forced an even larger trade deficit through the balance of payments mechanism we've described. The policy achieved the opposite of its intended effect.

This also highlights why focusing exclusively on trade-account measures like tariffs in Trump's second term would likely fail again. When faced with tariffs, trading partners have numerous ways to counteract these measures that go well beyond simple retaliatory tariffs. For example, monetary policy loosening can trigger currency depreciation via capital outflows that offset trade effects

The key insight is that in today's financially integrated world, any policy that focuses solely on trade flows while ignoring capital flows is likely to be ineffective or counterproductive. This suggests that successful trade policy must address both sides of the balance of payments equation.

The Politics of Capital Flows and Why Politicians Focus on Tariffs

The administration's public focus on tariffs rather than capital flow measures reflects political reality. Trade deficits and tariffs are concepts voters understand intuitively. Capital flows and balance of payments adjustments are not.

Most Americans, including policymakers, believe the U.S. needs foreign capital to fund its spending habits. The conventional wisdom holds that we're fortunate foreigners are willing to buy our debt. However, the evidence shows this gets the causality backward.

If the U.S. were truly dependent on attracting foreign capital to fund excessive spending, we would see two clear signs:

1. U.S. financial assets would underperform as we competed for scarce foreign capital

2. The dollar would weaken as our need for external funding grew

Instead, we see the opposite. U.S. financial assets have been among the world's best performing, and the dollar has remained exceptionally strong despite decades of trade deficits. This pattern is precisely what we'd expect when foreign demand for U.S. financial assets drives trade deficits, not the other way around.

History provides clear examples of countries that genuinely needed to attract foreign capital to fund trade deficits. They invariably faced weak currencies and poor asset returns, having to offer substantial yield premiums to entice foreign investors. The U.S. experience could not be more different.

While this reality makes capital account measures potentially more effective than tariffs, it also makes them harder to sell politically. Trump's rhetoric focuses on the more easily understood trade restrictions, even as his team appears to grasp the deeper dynamics at play.

Policy Options and Likely Outcomes

While markets remain focused on the prospect of tariffs, we expect a more sophisticated strategy that targets the root cause of trade imbalances: excessive capital inflows.

The administration has two broad paths available: negotiated adjustment through what we might call a 'Mar-a-Lago Accord', or unilateral action through capital flow restrictions. Both approaches would mark a decisive shift from previous policies that focused solely on trade flows.

The Mar-a-Lago Accord Scenario

Our base case envisions the administration pursuing coordinated adjustment with major trading partners, particularly China. Like the 1985 Plaza Accord, which engineered a major realignment of global currencies, this agreement would aim for orderly appreciation of surplus countries' currencies against the dollar.

Several factors make this approach likely. First, key administration officials, particularly Treasury Secretary nominee Scott Bessent, understand that currency adjustment rather than tariffs offers the clearest path to restoring U.S. manufacturing competitiveness. Second, the administration holds significant leverage through its ability to restrict foreign access to U.S. financial markets - a threat made credible by the sophisticated understanding of capital flows demonstrated by officials like Vice President-elect Vance.

The mechanics would likely involve agreed targets for currency appreciation combined with commitments from surplus countries to boost domestic demand. For China, this would accelerate its stated goal of transitioning from export-led to consumption-driven growth. While previous administrations have sought similar commitments, they lacked credible enforcement mechanisms. The threat of capital flow restrictions would provide this leverage.

Unilateral Action Scenario

If negotiations fail to produce meaningful adjustment, we expect the administration to move toward direct measures targeting capital inflows. The historical precedent exists - until 1984, the U.S. maintained a 30% withholding tax on foreign interest income. The elimination of this tax played a crucial role in enabling the explosion of global capital flows we've witnessed since.

Capital flow restrictions could take several forms:

1) Reinstating withholding taxes on foreign interest income

2) Taxes on foreign purchases of U.S. financial assets

3) Direct limits on foreign ownership in certain sectors

The effectiveness of these measures stems from a fundamental asymmetry in global trade: surplus countries must find somewhere to send their excess savings. While they can retaliate against tariffs through various means, they have far fewer options when faced with restrictions on their ability to export capital.

Consider China's position. Its economic model generates savings far exceeding domestic investment opportunities. These savings must be exported somewhere, and the U.S. financial system, with its depth and sophistication, has been the primary destination. If this outlet is restricted, China faces difficult choices: allow currency appreciation, accept higher unemployment as excess savings can't be exported, or undertake painful domestic reforms to boost consumption.

Market Implications

Either scenario - negotiated or unilateral adjustment - would have significant implications for financial markets, though perhaps not in the ways many expect.

While conventional wisdom suggests reduced foreign buying would drive bond yields significantly higher, this view misunderstands what drives bond yields. Treasury yields are primarily determined by the expected path of future Federal Reserve policy rates, not by foreign demand. Japan provides a clear example - despite decades of reduced foreign buying and even active selling of Japanese government bonds, yields have remained low, primarily reflecting Bank of Japan policy.

The more significant impact would likely be felt in currency markets, where the dollar would depreciate particularly against Asian currencies. This adjustment would be necessary and intended - it's the mechanism through which trade competitiveness would be restored.

Equity markets would face a complex adjustment. While a weaker dollar would benefit U.S. exporters and companies with significant domestic manufacturing operations, reduced foreign capital flows could affect overall market liquidity and valuations. Sectors and companies would likely experience divergent outcomes based on their position in global supply chains and their reliance on foreign versus domestic markets.

Real estate markets, particularly in major cities that have attracted significant foreign investment, could face more direct pressure as international capital flows diminish. Commercial real estate, already challenged by post-pandemic shifts in work patterns, could be particularly vulnerable to reduced foreign buying.

As Richard Koo recently noted, “What is happening in the stock market may not affect the living standards of the people directly, but inflation-adjusted housing prices, which have a direct impact on household finances, have soared 96.6%. The fact that the real wages of the ordinary Americans seeking to buy these houses have risen by only just over 15% makes it clear in many senses that their standard of living has declined. It should not be surprising that they are so unhappy with the current system.”

Since the early 1980s, U.S. household net worth has soared from around 350% of GDP to over 600%. This dramatic rise coincided with two transformative shifts in the global economy: the explosion in cross-border capital flows and the emergence of persistent U.S. trade deficits.

The timing is no coincidence. When foreign capital flows into U.S. financial markets but doesn't purchase American goods and services, it must instead buy existing assets - stocks, bonds, and real estate. Four decades of this persistent foreign buying has inflated asset values far above their historical relationship with the underlying economy.

If global trade imbalances reverse through the policies we've discussed, this ratio would likely begin normalizing - not necessarily through falling asset prices, but through faster GDP growth relative to asset values as U.S. manufacturing and exports revive. This rebalancing could be gradual under a negotiated adjustment or more abrupt if capital flow restrictions are imposed unilaterally.

Conclusion

The coming shift in U.S. trade policy reflects a deeper understanding of how modern global finance works. While markets remain focused on tariffs and trade restrictions, the real action will likely center on managing capital flows that have prevented natural economic adjustment for decades.

The new administration appears to grasp what previous ones missed: in today's financial system, trade imbalances persist because massive capital flows overwhelm traditional trade relationships. The U.S. runs persistent deficits not because it consumes too much or produces too little, but because it absorbs too much of the world's excess savings.

Policy success will require addressing this root cause. Either through negotiated adjustment - a Mar-a-Lago Accord - or unilateral capital flow restrictions, the goal is to reduce foreign purchases of U.S. financial assets and increase their purchases of U.S. goods and services.

The transition could be disruptive, but continuing current arrangements has become unsustainable. Surplus countries must eventually accept a reduction in their ability to export capital to U.S. financial markets. The U.S., as a deficit country, holds more leverage than many realize in forcing this adjustment.

For investors, this shift has profound implications. The era of persistent dollar strength despite trade deficits may be ending. A more competitive dollar would help restore balance to the U.S. economy, reviving manufacturing while allowing a more natural relationship between financial markets and real economic activity. The alternative - continuing to absorb the world's excess savings while hollowing out domestic industry - has become politically and economically untenable.

Thanks for your post. You write “ Therefore, when foreigners use their dollars to buy more US stocks or bonds, it automatically reduces US net exports of goods and services“. Without a currency adjustment, what’s the “ automatic “ mechanism that reduces US net exports?

Very interesting thoughts Michael -thanks for sharing. I stumbled upon your post just recently. Now if I compare the global tariff war the Trump administration started to your insights that both Vance and Bessent know better -how does this obvious contradiction resolve? Did they got overruled by some other tariff hardliners in the government or is this a sort of bluff to force trade partners at the table for such a Mar-A-Lago-accord?